Published October 2024. Data sourced from YCharts as of 10.8.2024.

Equity and fixed income markets had a strong third quarter, which concluded with a 50 basis point reduction in the fed funds rate amidst a healthy economic backdrop. The S&P 500 rose 5.9%, its fourth consecutive positive quarter and seventh of the last eight (FactSet). This quarter was unique compared to recent quarters though; technology and growth stocks underperformed while rate sensitive and cyclical stocks outperformed. Mag-7 names were mixed; TSLA (+32.2%) and AAPL (+10.8%) had good quarters, while GOOG (-8.7%) and MSFT (-3.6%) retreated. Energy stocks were lower amidst lower energy prices; the S&P Energy commodity Index was down 12.2%. Fixed income returns were strong, earning a year of return in one quarter as rates dropped in anticipation of the Fed cutting rates. The AGG was up 5.3%, but long duration instruments like Treasury bonds and IG corporate bonds performed the best as 10 and 30-year Treasury bond rates fell 55 and 37 bps, respectively. Crypto currencies were mixed; Bitcoin was up 7.9% but Ethereum was down over 21%.

Well, that was fast.

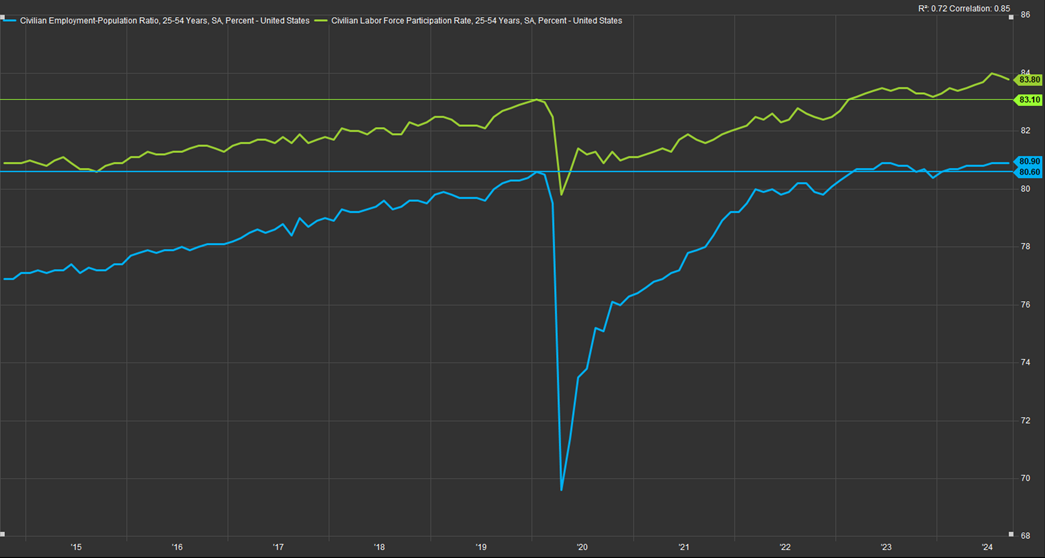

Last quarter, I wrote about three topics that received a lot of attention in Q3: labor market “weakness,” the widening discount between large cap and SMID stocks, and the negative term premium across the yield curve. For labor, I pointed out that the unemployment rate had fallen not because of increased layoffs or lower employment, but because of record immigration leading to labor force growth (new entrants). Since then, concerns over the labor market have retreated. The surge in initial jobless claims was short-lived, wage growth has remained above inflation, and the unemployment rate decreased to 4.1% from 4.3%. While jobs growth is slower than two years ago, we also have a tight labor market with fewer available workers; the working-age labor force participation (green) and employment (blue) rate surpassed 2019 levels in mid-2023 and hit new record highs in 2024 (see chart below from FactSet). A slower pace of hiring makes sense in an economy at full employment rather than a surplus of workers. To put a final pin it, aggregate wages and salaries have risen at a 6% YoY rate throughout 2024, well above inflation of 2.5-3%. The labor market looks healthy to me.

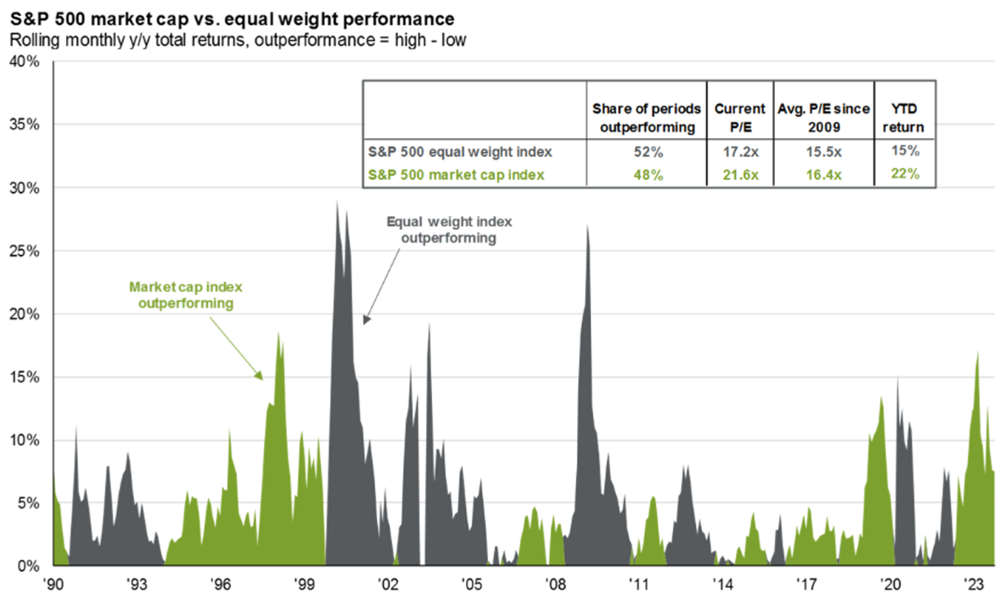

Small and mid-cap performance has also turned around. Both categories outperformed their large cap counterparts during Q3 amid the broadening of equity returns. The average stock in the S&P 500, represented by the ETF RSP, outperformed the S&P 500 by 360 bps. We witnessed this briefly in Q4 2023, but it simmered amidst poor economic and inflation sentiment earlier this year. Those concerns eased in Q3, with the first catalyst being the June CPI report released on July 11th. The Citi Economic Surprise Index, which tracks whether new data comes out better or worse than consensus expectations, hit a local bottom of -46 on that day; it ended the quarter flat and as of this writing is at +15. The return of “soft/no landing” consensus, tame inflation, and the start of the rate cutting cycle all helped the broad rally wake up last quarter; since then, small and mid-caps more than doubled the return of the S&P 500, and Mag-7 names were noticeable underperformers. A change in leadership from the concentrated mega-caps to other stocks under the surface has historical precedent in the early 2000s, which was the last time relative returns and valuations between large and small cap stocks were this wide. The graph below from JPMorgan shows the wax and wane of this historical relationship well and how the trend has been one-sided over the past few years but is starting to turn (notice the sharp drop recently). We expect this to continue.

The final topic I addressed last quarter was the inverted yield curve, or as I put it earlier, the “negative term premium.” Obviously, investors expect extra return to bear extra risk, such as interest rate and inflation risk, but yields on cash remain above yields on longer dated bonds as investors continue to expect further rate cuts. But the yield curve is becoming more normal; the 10-year yield crossed above the 2-year yield in early September, creating a positive term premium (for those rates) for the first time in over two years. This spread, now at six bps, is not enough to entice us to take duration risk; the yield curve continues to price in what we think are aggressive assumptions for Fed policy given the economic backdrop. We also believe current pricing ignores the risk of a higher terminal fed funds rate or a longer path to get there. Therefore, we continue to focus fixed income exposure between 1-7 year maturities, which we think gives investors acceptable return while insulating them from upside pressure on the long end.

Don’t underestimate continued growth.

Over the last two years, investors and market prices have gone back and forth between worry and relief. Worry that inflation was getting out of control, then relief in October of 2022 after it cooled quickly. Worry that the Fed was going to keep rates high indefinitely, followed by relief in October of last year as the Fed pivoted. Recently, the worry has been that the economy’s strength has run its course, and we are bound for recession. The “relief” is starting to set in as numerous economic data points surprise to the upside, including nonfarm payrolls, jobless claims, and a large upside revision to 2019-2023 real GDP and GDI. This can be seen in the recovery in the Citi Economic Surprise Index mentioned above and shown below (FactSet). The latest relief rally is helping equities have another stellar year. Worry still exists in the market. Above-average valuations remain a key concern, retail money market balances are $2.6 trillion and up 12% this year, and sentiment levels for consumers and businesses are at early 2023 levels despite meaningful economic progress since then.

Going into Q4, we consider a sustained economic expansion an achievable outcome. As we have said, the U.S. economy has already achieved a “soft landing” by avoiding recession over the last two years by means of a series of rolling recessions that have now normalized to a “typical” economic cycle. Thus, we may have already begun a new economic cycle. Our expected labor force and productivity growth of 2-3% a year can certainly sustain growth, especially when combined with near-term tailwinds. According to FactSet, corporate sentiment is uncharacteristically optimistic following a year of deceleration; “weak demand” mentions are also tracking at the lowest level in two years. A common theme I noticed in last quarters’ earnings calls was the large backlog of industrial and construction projects that were delayed in 2023-2024 due to expected recession, high rates, or the election, but are expected in 2025. According to Politico, only 30% of the funds in the Nov. 2021 Infrastructure Bill have been spent and electrification/grid investments are expected to be $1 trillion over the next 5 years to support growing power demand from new data centers and chip manufacturing facilities. Earnings growth estimates are thus strong across the board; the S&P 500 and the average stock is expected to grow earnings by 15% next year; small cap earnings growth is expected to be 20%. All these tailwinds while NOW-CAST GDP growth (via the Atlanta Fed) is tracking current growth at above 3.5%, we are at full employment, and the Fed is cutting rates.

The early innings of an economic recovery typically favor cyclical and smaller market-cap stocks, which by our assessment are the cheapest and most under-loved parts of the market. This is why we have been rebalancing allocations away from the high-flying Mag-7 stocks to everything else, which includes stocks that trade at more reasonable valuations, but also those that benefit from the secular trends mentioned above. We have also shortened up the maturity of fixed income allocations, given the massive move lower in long-term rates, which we believe is inconsistent with current economic performance and a “normal” term premium relative to cash. This composition of assets checks a lot of boxes for a framework looking to take advantage of intermediate term trends while managing potential downside risks.