Different markets call for different approaches to managing your portfolio. Should an investor take a passive approach through a fund designed to mirror the changes in a market index as a whole or actively manage the portfolio with stocks chosen individually? It depends.

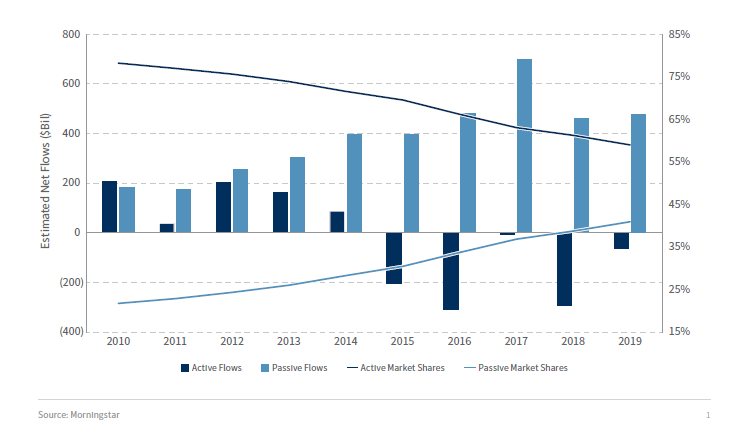

Over roughly the last decade, passively managed index funds have seen record inflows of investor capital, steadily taking market share from their actively managed counterparts. The chart below illustrates this trend, beginning in 2009.

It’s no coincidence that the boom in passive investment popularity coincided with the end of the Great Recession. Performance over that time has largely exceeded active investment performance, in part due to high correlations among sectors and companies regardless of underlying fundamentals. In addition, a handful of blue-chip technology companies have dominated U.S. stock market performance for much of the last 10 years.

Many investors have wondered whether active management is still valid given the relative outperformance of passively managed strategies (primarily, index funds) versus the average actively managed investment strategy. While it’s true that passive strategies tend to outperform in sustained bull markets, active managers often shine in choppy and bear markets. Though investors may favor one investment approach over the other, it’s not necessarily an either-or decision.

ACTIVE VS. PASSIVE INVESTMENT MANAGEMENT

In general, actively managed investment strategies attempt to outperform a broad market index by selecting the most attractive investment opportunities within a stated mandate. For example, an active manager’s mandate may be to outperform the S&P 500 by investing in 20 to 30 large U.S. company stocks. Typically, one or more portfolio managers are responsible for selecting these investments and performance is based on the manager’s ability to pick winners. On the other hand, passive investment strategies usually try to match the performance of a broad market index – for example, the S&P 500 – by owning all or a sampling of the investments in the benchmark. These strategies are typically driven by computer algorithms, and their performance doesn’t rely on the expertise of a portfolio manager – a distinction that also makes passive investments less expensive than their active counterparts.

PERFORMANCE PATTERNS

Investors who oppose active management argue that in certain asset classes, active managers cannot consistently outperform their respective broad market benchmark. Some segments of the market – for example, large company stocks in the United States – are highly covered by analysts, making information on these stocks readily available. Therefore, it’s difficult for any one investment manager to have stock-specific information that gives them an edge over the competition. Proponents of passive investments argue that in these asset classes, a low-fee index-tracking strategy is more appropriate.

While this argument certainly has its merits, supporters of active management believe that in certain market environments – primarily volatile markets and bear markets – active managers have a better chance of outperforming. This is because managers that have the flexibility to raise cash, invest more heavily in certain sectors of the market and select superior investments typically fare better than passive strategies in periods of market distress.

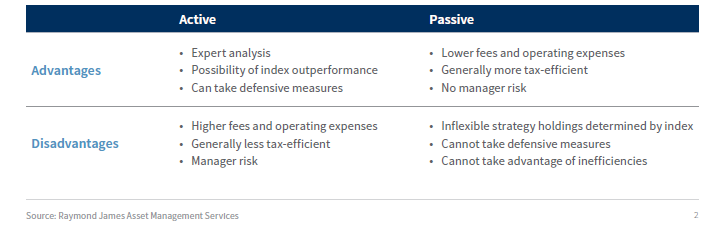

PROS AND CONS

The table below provides a high-level summary of the advantages and limitations of each investment approach.

NEXT STEPS

- Consult your plan’s fund lineup to see whether actively managed or passive investment strategies are available, or both.

- Given that active and passive investment strategies are better suited to different market environments, both investment styles may have a place within a retirement portfolio.

- If you are unsure which investments to select, talk to your financial advisor. In addition, your 401(k) plan’s record-keeper may have educational resources and tools to help you determine which investment approach is most appropriate given your retirement goals.

Investing involves risk and investors may incur a profit or a loss. The S&P 500 is an un-managed index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance.