Investment behavior of retirement investors historically consistent, regardless of stock market direction, glide path type, or time horizon.

Key Takeaways

- The savings behavior of target date strategy investors in workplace retirement plans has been consistent over time, even during episodic stock market declines.

- The percentage of investors exchanging out of target date strategies during recent stock market declines was low regardless of which type of glide path was used, though investors in a strategy with a “through” glide path (reaching the most conservative stock allocation several years into retirement) were more likely to remain invested than those in a “to” glide path (reaching the most conservative stock allocation at the date of retirement).

- Workplace plan participants who were auto-enrolled into a target date strategy via their plan were more likely to stay invested than those who opted into a target date strategy by choice.

Target date strategies were launched 20 years ago as a single investment option designed to help investors who did not have the skill, will, or time to identify and manage an age-based asset allocation over an extended horizon. Because staying invested, particularly during declining markets, is an important tenet of long-term investing, we analyzed the behavior among target date investors in retirement plans under administration by Fidelity Investments to determine how investors reacted during recent U.S. stock market declines. The following article outlines the key findings of our study.

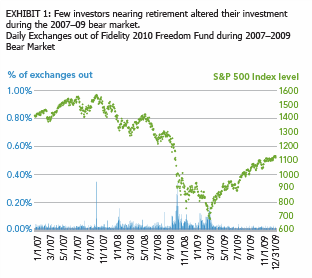

Based on all actively employed participants in defined contribution plans administered by Fidelity who were 100% invested in Fidelity’s Freedom 2010 Fund during the prior month, where participant ages fall within a five-year window of projected retirement in 2010. Daily exchanges out includes any full or partial exchange. S&P 500 Index data represents daily closing price. Fidelity data, as of Dec. 31, 2015.

Target date strategy investors remained engaged during 2007–2009 bear market

Looking at active participants in defined contribution (workplace) plans, we found that most target date strategy investors maintained their exposure during major stock market declines, and this behavior was consistent regardless of the investment horizon indicated by the target date strategies. For example, during the 2007–2009 bear market, the highest percentage of daily exchanges out of Fidelity’s 2010 target date strategy was low—less than one-half of one percent of all active participants (Exhibit 1). Presumably, this bear market occurred close to a planned retirement date for many participants holding the 2010 target date strategy, yet an overwhelmingly large percentage of them remained invested. Other periods featuring short-term stock declines, such as in the fall of 2015, showed even fewer exchanges for this investor group near retirement.

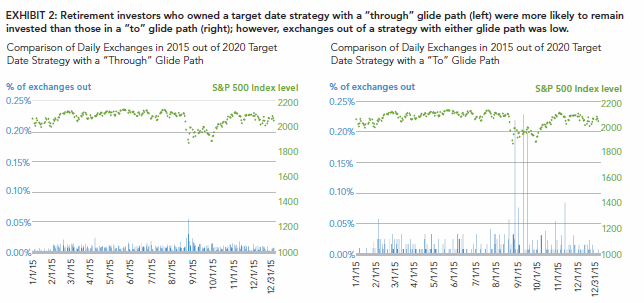

Comparing participant behavior in different glide paths during 2015 stock market downturn

We also evaluated whether target date strategy investors who were aligned with a “through” glide path—where the strategic allocation reaches its most conservative mix (lowest stock exposure) a number of years into retirement—were more or less likely to make an exchange out of their strategy than investors in a “to” glide path, which reaches its most conservative allocation at a specified retirement age.1 Looking at 2020 target date strategies during the stock market downturn in the fall of 2015, our analysis showed that investors in the “to” glide path of a 2020 target date strategy were four to five times more likely to make an exchange out of the strategy than those in a “through” glide path during this period (Exhibit 2). It’s unclear from the data why this pattern exists, but it’s worth monitoring going forward. Importantly, however, the number of exchanges among investors in each type of glide path was low during this period, indicating that a glide path choice did not appear to drive many target date investors out of their planned, long-term investment.

EXHIBIT 2: Retirement investors who owned a target date strategy with a “through” glide path (left) were more likely to remain invested than those in a “to” glide path (right); however, exchanges out of a strategy with either glide path was low.

Based on all actively employed participants in defined contribution plans administered by Fidelity who were 100% invested in a single 2020 target date fund during the prior month, where participant ages fall within a five-year window of projected retirement in 2020. “Through” glide path represented by participant investors in Fidelity’s Freedom 2020 Fund. “To” glide path represented by participant investors in a 2020 target date mutual fund using a “to” glide path, according to the investment provider and Morningstar Inc. Daily exchanges out includes any full or partial exchange. S&P 500 Index data represents daily closing price. Fidelity data, as of Dec. 31, 2015.

Investors auto-enrolled into a target date strategy were more likely to stay invested during 2007–09 bear market

Employees who were automatically enrolled into their workplace retirement plan were less likely to exchange

out of their target date strategy during a bear market than those who opted into a target date strategy by choice, our findings showed. During the 2007–2009 bear market period, auto-enrolled investors exchanged out of their 2010 target date strategy at a peak daily exchange rate of less than 0.20%, while those who were not enrolled automatically and chose to purchase a target date strategy on their own had a peak daily exchange rate of nearly 0.50%. Although exchange rates for both investor groups remained low, those who were automatically enrolled were more likely to stay the course during downturn.

For plan sponsors, these results indicate that workplace plan designs with an auto-enrollment feature may be more likely, on the margin, to keep target date strategy participants invested in their strategy during volatile markets. A recent industry study indicated that investors in target date strategies historically have experienced realized returns quite similar to the actual published returns of their strategy, due to their systematic investing via workplace retirement plans and their ability to maintain their investment strategy through market downturns.2 In comparison, the returns realized by investors owning strategies in other categories were significantly lower than the actual returns of the strategies, and this return gap was largely attributed to poor investor behavior decisions, such as exchanging out of their strategies at the wrong time.

Based on all actively employed participants in corporate defined contribution plans (including advisor-sold DC) administered by Fidelity who were actively employed by a plan sponsor and 100% invested in the indicated target family for the indicated year (2010) during the prior month, whose ages are consistent with an age-based allocation within a five-year window of projected retirement. Auto-enrollment: participants who were auto-enrolled into the stated target date fund by their plan. Daily exchanges out includes any full or partial exchange. Fidelity data, as of Dec. 31, 2015.

Final thoughts: Many target date strategy investors follow the plan

Using target date strategies to achieve a retirement income objective requires both consistent savings behavior on behalf of workplace plan participants, and risk-appropriate investment returns from an investment manager (see Fidelity Leadership Series paper “Retirement Study: Effective Plan Design and Glide Path Choices Led to Better Outcomes”). A long time horizon can serve as an advantage for retirement investors, provided savings discipline is maintained, particulary during volatile or declining markets. Our analysis indicates most target date investors have maintained prudent investment behavior during episodic stock market downturns, and that discipline is likely to help target date strategy investors seeking to achieve a desired standard of living in retirement.

Authors

Mathew R. Jensen, CFA l Director, Target Date Strategies

Mathew Jensen is the director of target date strategies in the Global Asset Allocation (GAA) group at Fidelity Investments. Mr. Jensen leads investment strategy execution and product design and innovation across the company’s target date offerings, and directs target date investment research and thought leadership.

Brian Dewhirst, PhD l Senior Quantitative Analyst, WI Finance Customer Analytics Group

Brian Dewhirst is a senior quantitative analyst in the Workplace Investing (WI) group at Fidelity Investments. Dr. Dewhirst’s role involves maintaining a dataset used in cross-functional collaboration with other business units related to WI customer behavior, performing analysis of that dataset, and producing analytics related to defined contribution investment trends.

Christopher Moeder, CFA, CFP l Senior Research Analyst

Christopher Moeder is a team leader within the Global Asset Allocation group at Fidelity Investments. In this role, Mr. Moeder is a member of the Asset Allocation Research Team (AART), which conducts economic, funda-mental, and quantitative research to develop asset allocation recommen-dations for Fidelity’s portfolio managers and investment teams.

Fidelity Thought Leadership Vice President Kevin Lavelle provided editorial direction for this article.

Endnotes

1. The 2015 period was chosen to illustrate investor behavior primarily because an adequate sample size of data was not available for “to” glide paths during the 2007–09 bear market period. Several investment management companies launched target date funds with “to” glide paths after the 2007–09 bear market. 2. “Mind the Gap 2016,” Morningstar Inc., June 10, 2016.

Before investing in any mutual fund, please carefully consider the investment objectives, risks, charges, and expenses. For this

and other information, contact Fidelity for a free prospectus or, if available, a summary prospectus. Please read it carefully.

Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or solicitation to buy or sell any securities. Views expressed are as of the date indicated, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the authors and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

Investing involves risk, including the risk of loss. • Past performance is no guarantee of future results. • Neither asset allocation nor diversification ensures a profit or guarantees against a loss.

Unless otherwise disclosed to you, in providing this information, Fidelity is not undertaking to provide impartial investment advice, or to give advice in a fiduciary capacity, in connection with any investment or transaction described herein. Fiduciaries are solely responsible for exercising independent judgment in evaluating any transaction(s) and are assumed to be capable of evaluating investment risks independently, both in general and with regard to particular transactions and investment strategies. Fidelity has a financial interest in any transaction(s) that fiduciaries, and if applicable, their clients, may enter into involving Fidelity’s products or services. • Investment decisions should be based on

an individual’s own goals, time horizon, and tolerance for risk. Nothing in this content should be considered to be legal or tax advice and you are encouraged to consult your own lawyer, accountant, or other advisor before making any financial decision. • Information presented here is general in nature and should not be construed as legal advice or opinion. Plan sponsors must decide for themselves which investment options are appropriate for their plan.

Target date portfolios are designed for investors expecting to retire around the year indicated in each portfolio’s name. Each portfolio is managed to gradually become more conservative over time as it approaches its target date. The investment risk of each target date portfolio changes over time as the portfolio’s asset allocation changes. The portfolios are subject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad, and may be subject to risks associated with investing in high-yield, small cap, commodity-linked, and foreign securities. Principal invested is not guaranteed at any time, including at or after the portfolios’ target dates. • Target date portfolios are designed to help achieve the retirement objectives of a large percentage of individuals, but the stated objectives may not be entirely applicable to all investors due to varying individual circumstances, including retirement savings plan contribution limitations.

Fidelity’s “through” glide path may differ somewhat from those of other target date strategies, which could influence the results of the analysis in this article.

If receiving this piece through your relationship with Fidelity Clearing and Custody Solutions or Fidelity Capital Markets, this publication is for institutional investor or investment professional use only. Clearing, custody or other brokerage services are provided through National Financial Services LLC or Fidelity Brokerage Services LLC, Member NYSE, SIPC.

Download Attachment: Download Whitepaper