The benefits of calculating compensation right the first time far outweigh the headache and costs of making corrections after your plan year has ended. That’s why it’s important that you understand the different types of compensation and how they are used to administer your plan.

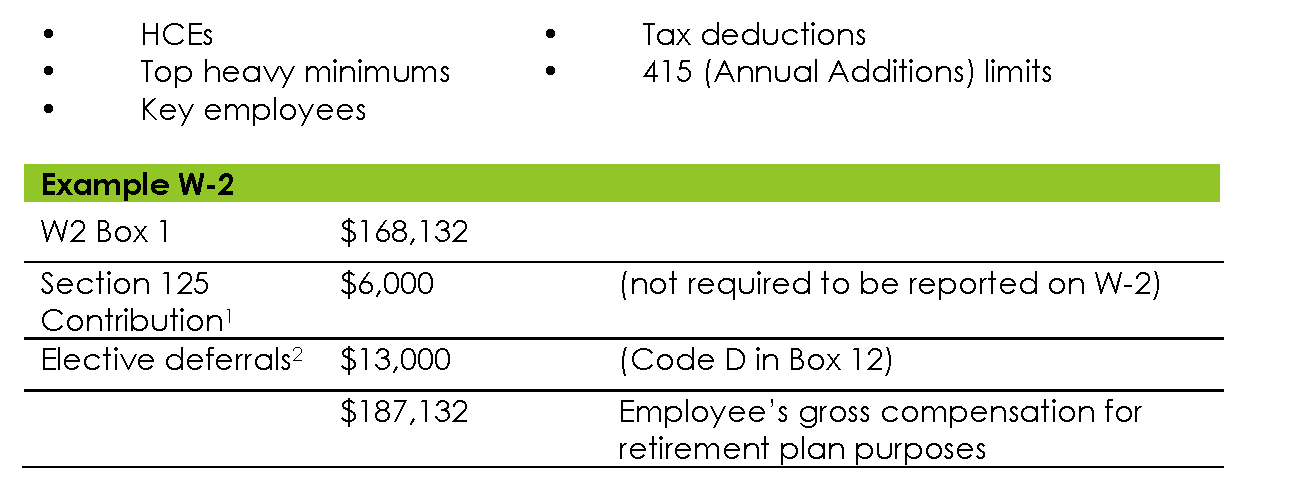

Compensation information is used for many purposes, including: determination of employee and employer contribution amounts, required IRS non-discrimination testing and identification of Highly Compensated Employees (HCEs) from year to year. Generally, there are two types of compensation to consider:

1. Gross compensation and 2. Plan compensation.

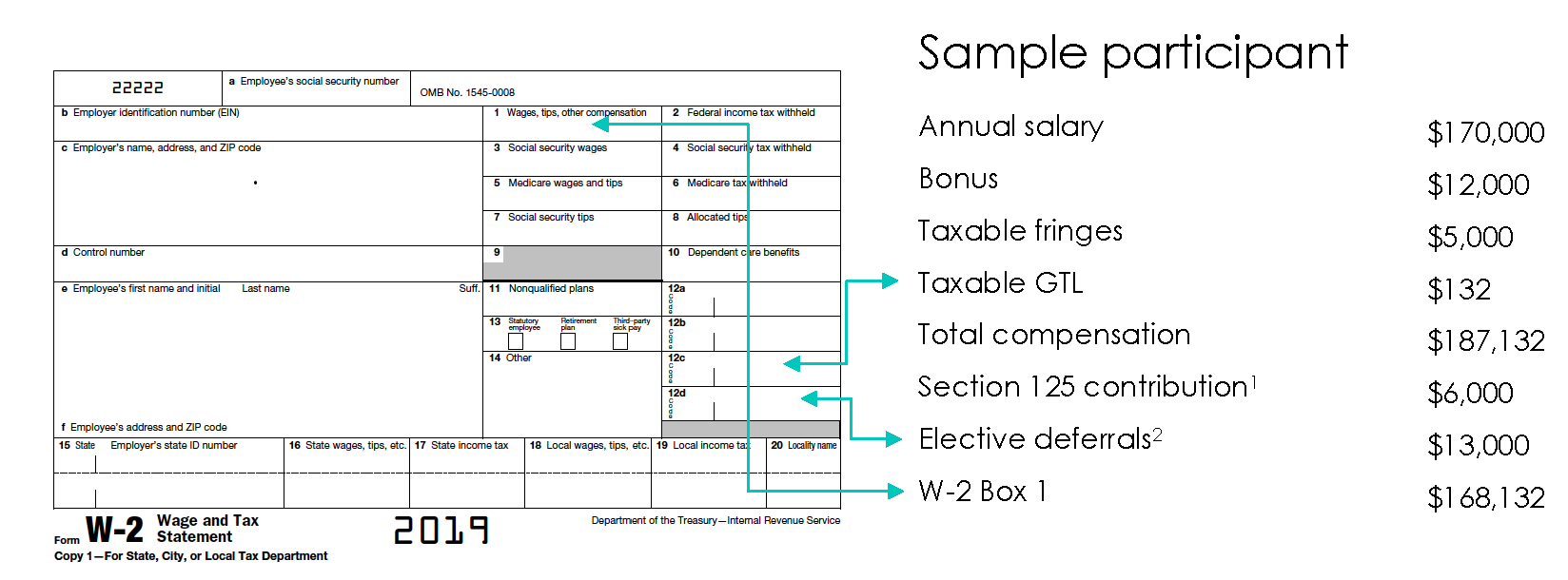

Let’s take a look at some examples using the following payroll data:

Gross compensation

Gross compensation is the same for most plans and is defined as total taxable compensation found in Box 1 of the W-2 plus any non-taxable compensation such as deferrals to a retirement plan or salary reductions to a cafeteria plan. If your plan uses a different definition for compensation, your gross compensation may vary slightly. For example, if your plan compensation is based on 3401(a) wage withholding, the gross compensation will be similar to the W-2 but will not include taxable group term life or taxable reimbursements reportable on the W-2 but not subject to wage withholding.

Gross compensation may be used to determine:

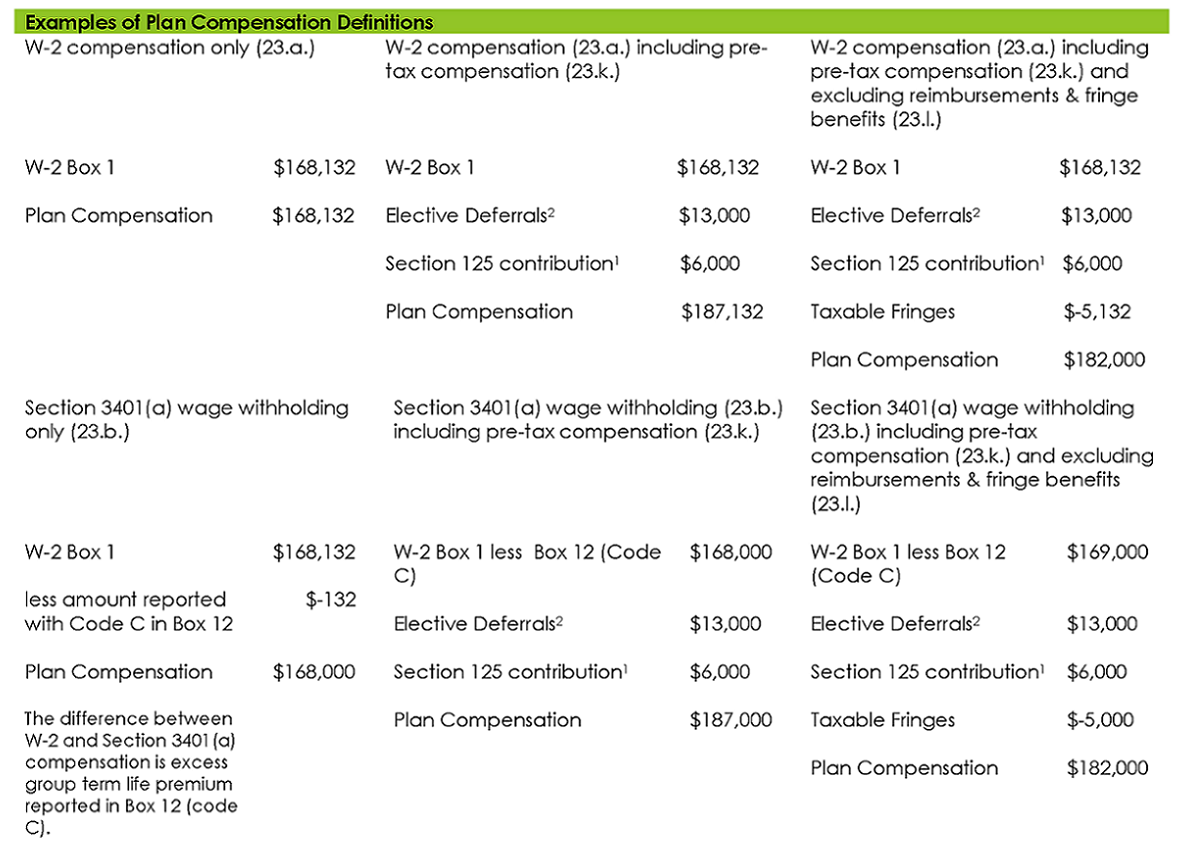

Plan compensation

Plan compensation is specific to each retirement plan. It is defined by you, the employer, based on choices made in the plan document. Your plan most likely defines compensation as either W-2 or wages subject to withholding

(3401(a)). Additionally, this compensation may be adjusted to include or exclude certain types of cash or non-cash compensation (e.g., pre-tax contributions, fringe benefits).

Plan compensation may be used to determine:

The following examples illustrate typical plan compensation definitions using the sample payroll data from side one. The applicable plan document section for the Minnesota Life 401(k) volume submitter is provided for your reference in the parenthesis (e.g., 23.a.).

- Section 125 contributions are not subject to any withholding taxes (including FICA) and are not required to be reported on the W-2.

- Elective deferrals are pre-tax contributions made to a 401(k), 403(b) or 457 plan and are reported in Box 12 of the W-2.

This information must be located from other payroll records.

This information should not be considered as tax advice. You should consult your tax advisor regarding your own tax situation.

- Your plan may use one definition of plan compensation to calculate deferrals and match and another to calculate your profit-sharing contribution. If so, you will need to report both types of plan compensation, along with gross compensation, to Securian.

- Your plan’s compensation definition may exclude certain types of compensation such as bonuses, commission or overtime (see section 23.p,q,r). If so, start from the appropriate example above based on how your plan document is completed and subtract the appropriate exclusions.