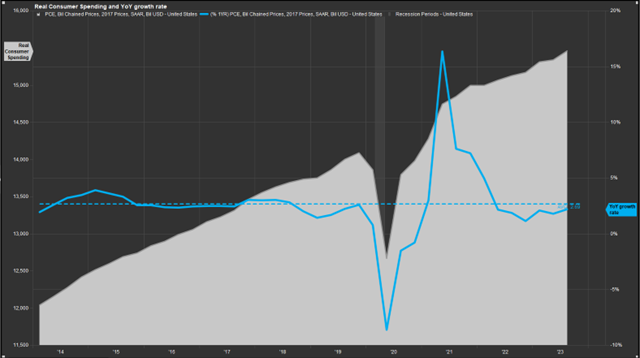

They say history tends to repeat itself, and in 2023, it did. Historically, investors that stay invested through severe market downturns are rewarded because prices inevitably rebound, and that’s exactly what happened in 2023. As a quick review, the S&P 500 fell 24% at its lowest in 2022; since then, it’s up over 35%, including a gain of 26.3% in 2023. That’s quite a turnaround in just over a year, and certainly not what most market participants were expecting. Markets were expecting inflation to be persistent, the labor market to deteriorate, and for higher interest rates to dampen economic activity. As it turns out, the labor market was exceptionally strong; the unemployment rate remained very low at 3.7%, 2.7 million jobs were added, and wages grew more than inflation. While inflation is not down to the 2%-levels we grew accustomed to after the financial crisis, 3.4% is getting close, and half of what it was going into 2023. Economic activity also remained at healthy levels; albeit, with some weakness in areas such as real estate, manufacturing, and trucking. Consumer spending, which accounts for almost 70% of the U.S. economy’s total spending, surprised to the upside last year. As you can see on the blue line in the chart below, inflation-adjusted consumer spending resumed its pre-pandemic upward trend. While growth slowed after the massive stimulus in 2021, it did not dip negatively, but rather normalized back to its 10-year average of around 2.7%. The strength of the labor market and consumer have many investors believing the hype of a “soft landing,” and is a large contributor to the strong rally we experienced in Q4.

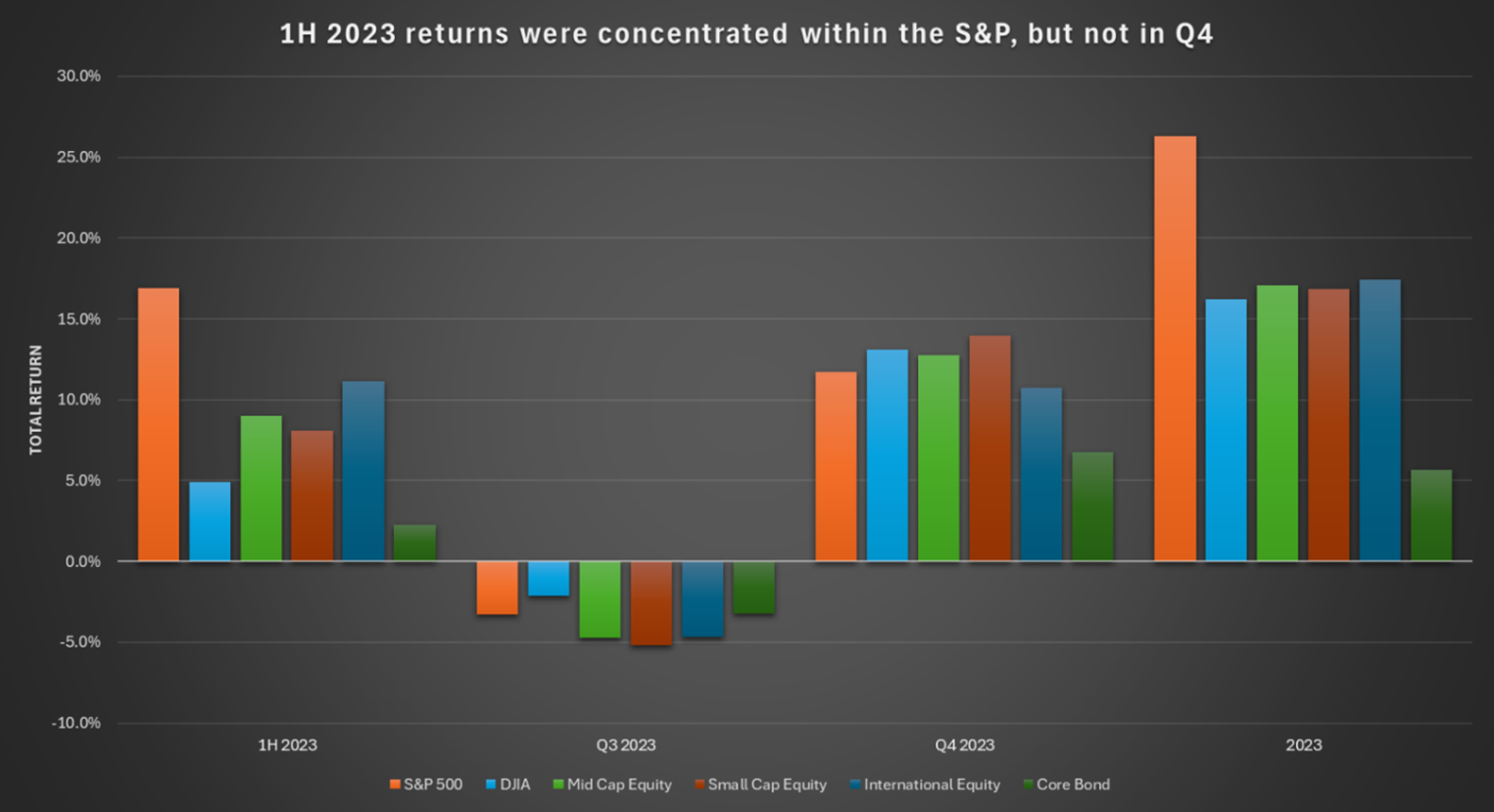

While these outcomes are known now, they were a primary worry for investors throughout most of 2023, which held back market performance in the first half. As we pointed out in previous newsletters, equity market returns were concentrated in just a few, enormous stocks, which made the market cap weighted indices, like the S&P 500 and Nasdaq, outperform the average stock within those indices. This created an illusion of strength within equity markets but in reality, was only strength in seven large tech stocks. For instance, the S&P was up nearly 17% in the first half, but the Dow Jones was only up 5%; the Russell 2000, an index that tracks the performance of small stocks, also returned less than half of the S&P’s return. However, as market sentiment regarding the economy, inflation, and perhaps most importantly, Federal Reserve policy improved, the other 493 stocks joined the market rally. Below is a chart showing asset class returns for the first half, Q3, Q4, and all of 2023. As you can see, returns in Q4 were much broader than in the 1st half, with small and mid-cap equities outperforming; however, they still significantly underperformed the S&P 500 in 2023. This Q4 broad market rally helped portfolio returns tremendously; most balanced allocations had higher than average returns last year.

Looking forward, we are encouraged by these developments. A broadening market rally, led by cyclical stocks such as small caps or financials, is typically a sign of an early stage bull market. However, markets are often overzealous to price in new information, and we think that may be happening today. For example, as inflation came down in 2023, investors started to expect the Federal Reserve to begin cutting rates in an effort to keep “real” interest rates the same. As of the end of 2023, markets were pricing in 150 bps of cuts, whereas the Fed only expects to cut rates 75 bps. Moreover, market prices relative to fundamentals remain on the high end of historical averages and earnings growth expectations (11% for 2024) are high relative to economic growth expectations (Consensus real GDP estimates are for 1.3%). It’s possible we pulled forward some returns from 2024 into Q4 of 2023, and therefore, we may enter a digestion period where market fundamentals catch up to market prices. However, this does not mean we do not see opportunity in the market. Much of the premium valuation in equity markets is due to the mega-cap names that dominate the indices. On the other hand, mid and small cap stocks are trading at a discount relative to where they typically trade and relative to large caps. If we have successfully avoided a recession, which has become market consensus, we think the rally will continue to broaden out and these smaller stocks will continue to outperform their large cap counterparts. We also remain long term bullish on equities as an asset class. Productivity growth from artificial intelligence is likely to boost economic growth broadly; a rising tide lifts all boats. However, we see opportunities not just in the companies that sell A.I. software, but in their vendors, users, and unintended beneficiaries. According to IT consulting firm Gartner, A.I. could use 3.5% of the world’s total electricity generation by 2030. Where is that additional power coming from and how will it be distributed to the areas requiring the highest power consumption for applications and data centers? Companies deploying A.I. will reduce costs, become more efficient in their operations, and free up additional bandwidth for additional revenue growth opportunities. Vendors of electronic components, chips, and hardware will benefit from increased adoption and use. Data owners and providers will see higher value use cases for their data as it’s fed into A.I.-based large language models. We are invested in all these trends and believe they will deliver investors superior long-term performance regardless of what happens with the Fed or the economy in 2024.

While we maintain a long term perspective in markets, we remain acutely aware of intermediate term catalysts and risks. When markets pull forward return due to optimistic expectations, we prefer to rebalance portfolios, trim winnings, and redeploy them into assets that have better future risk/reward opportunities. We think bonds are an asset that has an attractive set up in this regard, and with higher interest rates, bonds can finally contribute to portfolio growth. Additionally, bonds have about a third of the risk of stocks and have asymmetric upside potential over the next 12-18 months as interest rates normalize. This opportunity is more attractive in an environment in which equities may have pulled forward returns. We believe equities remain the best vehicle for long-term wealth creation, but the returns are often volatile and entering the market at a time when optimism is at highs is risky. Nevertheless, we caution investors against trading frequently, timing markets, or chasing return; and instead recommend staying invested while rebalancing as needed. As the late Charlie Munger, business partner of Warren Buffet, said, “The big money is not in the buying and the selling but in the waiting.”